public procurement effectiveness via bibliographic and

case studies is performed. As a result, the majority of methods cover four

components of assessing the public procurement efficiency - targeted

efficiency, cost-effectiveness, organizational efficiency, efficiency of budget

expenditures for public procurement. This does not provide an assessment of the

automated systems’ impact on the procurement procedures results and on possible

savings due to the use of certain procurement procedures. To comprehensively

assess the procurement efficiency in e-bidding, the authors propose considering

four key risks: the risk of cancellation of the procurement procedure, the risk

that the procurement procedure will not take place, the risk of appealing the

procurement, the risk of disqualification. As a result of risks calculations

under the sub-threshold and above-threshold procurement, individual values of

risks and their aggregate indicator are determined. This will adjust the scope

of audit procedures to verify individual procurements and identify weaknesses

in the procurement management system. We believe that the methodology of auditing the

procurement effectiveness, taking into account the quantitative and qualitative

parameters of procurement risks, will be a useful audit tool to determine the

effectiveness of the use of public funds under individual procurements and

identify areas of cost-effectiveness

for the state budget funds.

Keywords: Public Procurement; Risks; Audit; Audit Assessment;

Efficiency; Finance; Enterprises

1.

INTRODUCTION

National economies have recently

been negatively affected by pandemics and quarantine measures. The negative

dynamics of the revenue side of the budget and the forced reduction of

expenditures necessitate a more careful approach to spending on procurement for

the needs of the state. Taxpayers who face the threat of increasing taxes and

fees and/or cutting services hope that the state budget expenditures on the

purchase of goods, works and services will be accompanied by the effective

management of taxpayers’ funds. This is not always the case. Recent advances in

the public procurement theory suggest that complex auctioning schemes create

opportunities for collusion and corruption (Lambert-Mogiliansky & Sonin,

2006).

Audits aimed at assessing the value

for money (VfM), which emerged in the late 70’s of the twentieth century in

response to the economic crisis and the budget deficit of the world (Pollitt et

al., 1999) began determining the efficiency of use in addition to legality.

Examining the types and forms of auditing (external, internal, public and

private (Bowerman, Raby & Humphrey, 2000), considered that

auditing is only one aspect of a broader but a rapidly evolving “performance

measurement society” that includes other important elements, which include

increased inspection and self-assessment. (Mayne &

Ontario, 2006) divide the purpose of audit and evaluation. Examining the

essence of performance audits, these authors name the result of the

methodologies used as one of the difficulties in fulfilling their roles to the

public sector.

The main task of the performance

audit, as one of the types of public audit is a constant and comprehensive

audit of three “E” - economy, efficiency and effectiveness (McCrae & Vada, 1997) of public procurement is carried out by all higher institutions of

public audit.

Increasing the analytical potential

of the audit in the current situation is an important direction in the

development of its methodology (Slobodyanik, Kondriuk & Haibura, 2019).

Mega-trends that will change the way

we do business in the next decade will not only require a rethinking of the

vision of procurement, make the necessary changes in their strategy, but also

create the conditions for changing methods of assessing efficiency and

effectiveness. Among the most important modernizing influences are the use of

big data and the global network, the new role of procurement in decision-making

based on this data (Spiller et al., 2013) and volatility as a new norm:

transfer of supply risk to competitive advantage (Spiller et al., 2013).

Adi and Dutil (2018) note the presence of asymmetry in the selection of objects of

performance evaluations, when many ministries are underestimated and others are

systematically overestimated. Therefore, increasing the productivity of the

audit organizations themselves is also in the application of more acceptable

criteria for the selection of the object and the implementation of assessments

according to modern adapted methods.

The audit results will help raising

public awareness about the results of assessing the effectiveness of the public

funds use in organized bidding.

2.

LITERATURE REVIEW

In the modern economic literature,

research on the category of “efficiency” and diverse methods and approaches to

its evaluation are widely presented. Research on performance analysis can be

divided into two main categories: (a) research related to the development of

regulatory decision-making procedures; and (b) those that discuss the

application of regulations to empirical data (Kroll & Levy, 1980). The main problems of analytical audit

evaluation of the results of procurement procedures in real life have received

limited attention in the theoretical literature.

Our contribution offers an

integrative nature of the audit evaluation methodology of the procurement

procedures effectiveness, which links the evaluation indicators of the three

“E” with the procurement risks. The effectiveness

of public procurement depends on a combination of factors: regulatory framework

for procurement, macroeconomic and political processes, the degree of

saturation of commodity markets, professionalism of customers, the adequacy of

the formulation of conditions and features of structural diversity of public

procurement.

The study of literature sources

showed a variety of approaches to assessing the effectiveness of procurement,

as well as the lack of consensus on the methodology of its implementation. This

diversity of approaches is explained by the fact that in Ukraine there is no

single methodology for assessment, including those defined by regulations.

Thus, some scientists in assessing the effectiveness of public procurement take

into account the calculation of the absolute and relative effect of public

procurement by comparing prices in a single competition (Methodological, 2008).

The method of Lapin, Kiseleva and Kumundzhieva (2016) is an example of such a technique,

which is designed to evaluate the activities of customers in the field of

public procurement. The researchers suggests calculating

two indicators: cost-effectiveness and the validity of the initial contract

price. Cost-effectiveness is calculated as the difference between the initial

(maximum) contract price and the price at which the contract is concluded. The second indicator - the assessment of the

validity of the initial (maximum) contract price is determined by the deviation

of the initial (maximum) contract price, which is stated by the customer, from

the average contract price offered by the bidders. The researchers proposes, in addition to

savings, i.e. the difference between the initial (maximum) contract price and

the price at which the contract is concluded, to evaluate the validity of the

initial (maximum) contract price as a deviation of the initial (maximum)

contract price from the average contract price, offered by the participants of

the order.

In our opinion, this approach has a

number of disadvantages. Thus, comparing the contract price with the average

price of suppliers’ bids, it is possible to determine the “effectiveness of the

tender within its participants”, but with a small number of such participants,

and even more so in case of conspiracy, the resulting performance evaluation

will be ineffective.

Ivanova (2010) proposes estimating

the savings in public procurement as the difference between the sum of the

average bid prices of suppliers and the sum of the bid prices for which the

contract is concluded and to determine such an indicator for each sector of

public procurement separately.

In addition, the scientist’s method

involves assessing the feasibility of determining the initial price of

contracts as a deviation from the average savings in the industry. We believe

that the comparison of the final value of the contract and the market price for

similar goods is a more acceptable indicator, in our opinion. However, in this

case, determining such a market price can be quite problematic. We will explain

why.

The market price is calculated on

the basis of information about the concluded identical agreements with

homogeneous goods, works or services. Thus, in most cases, customers use the

information posted on the websites of potential suppliers, and accordingly on

the basis of such data and determine the average market price. In the case of

impossibility to determine the market value of the order, and this is usually a

common practice in the procurement of works or services, then customers use the

cost method of determining the price.

In practice, there is another option

for determining the comparative efficiency of the order, namely on the basis of

contract prices for previous tenders. The

task of the customer is to develop and implement effective processes for

evaluating suppliers and determining the criteria for the winner (Sollish &

Semanik, 2012), which determines the prerequisites for

effective procurement. However, the disadvantage of this approach is that it

does not take into account the transaction costs of customers and does not

reflect changes in prices for such goods. In addition, it is clear that some

groups of goods may become cheaper over time, while others may become more

expensive.

In our opinion, the main

disadvantage of methods for assessing the public procurement effectiveness is

that they are based solely on price indicators. Therefore, the qualitative

characteristics of goods, works and services purchased on a competitive basis

are ignored, thus losing the meaning of such a competition. Moreover, the

evaluation of the public procurement effectiveness is not taken into account at

all. The latter comes down only to determining a monetary efficiency.

The authors evaluate cost models for materials,

consumables, and equipment in order to examine the potential cost savings from

specific procurement procedures. The results of the cost model show that the

use of competitive tenders, procurement calendars, central warehouses and lists

of tenderers is associated with significant cost savings (Duncombe & Searcy, 2007).

We should agree with the thought of

certain scientists on the need to take into account the assessment of the

public procurement quality, in other words, the level of the consumer’s

satisfaction with the services, works, or the delivery of goods, if “efficiency

depends on the value and productivity perceived by the consumer” (Karlöf, 1996).

Such interpretation can be

considered to be true, taking into account that quality is an indicator of the

sufficiency of the product and service’s power, which is responsible for the

assessment of the consumer’s satisfaction quality, in accordance with the goal

of that particular commodity. In this case, quality assessment is primarily a

diagnosis of the properties of usefulness and reliability, outlined by the

customer for the delivered goods or work and services performed. However, in

our opinion, this approach has its drawbacks, as there are some difficulties

with such an assessment.

So, according to the theory of

benefits, it seems that all benefits are classified into the inspectorate,

experimental and fiducial. A more detailed qualification allows the inspection

goods to be featuring such characteristics that may be defined only after the

delivery.

Specific features of experimental

benefits provide additional characteristics, as it is possible to reconfigure

it for less than an hour to get specific goods. In this case, fiducial goods

are a type of goods, the evaluation of which is characterized by a subjective

nature.

Therefore, given the above, it

should be noted that the time gap can serve as an important point in the

process of qualitative evaluation of efficiency.

A group of scientists - proponents

of a slightly different position, propose using the criteria of economy,

productivity of resources used, cost-effectiveness, taking into account the

time factor, with a thorough analysis of the type, conditions and completeness

of contracts (Nesterovich, 2008), evaluate the implementation of planned

indicators (Karlöf, 1996), which allows determining the

degree of goals’ achievement.

3.

DATA AND METHODOLOGY

The main input data parameters that

were used to test the hypothesis of the possibility and feasibility of using

risks in assessing the effectiveness of public procurement for audit purposes,

are formed in the open e-procurement system Prozorro (2020).

The time range of the study consists

of the interval 2018-2019 in terms of procurement data for each month. With regard to the choice of research methods,

the key task is the development of such arrays of indicators that allow

calculations of risks using both quantitative and qualitative parameters.

Quantitative risk parameters were

calculated using calculations of probabilistic indicators of procurement risk

assessment, such as the ratio of the number of relevant procedures to the total

number of procurement procedures (Table 1). Statistical methods were used for

cost assessments and calculation of the aggregate indicator of public

procurement risk (Table 1).

Table 1: The main indicators that

characterize the effectiveness of public procurement

|

No

|

Name of the

indicator

|

Method of calculating the indicator

|

|

Probabilistic indicators of public procurement risk

assessment

|

|

1.

|

Probability of cancellation of the procurement procedure

|

Number of canceled procedures / Total number of procedures

|

|

2.

|

Probability that the procurement procedure will not take place

|

Number of procedures that did not take place / Total number of

procedures

|

|

3.

|

Probability of appealing the procurement procedure

|

Number of complaints satisfied / Total number of procedures

|

|

4.

|

Probability of disqualification of the participant

|

Number of price offers of the disqualified participants / Total number

of price offers

|

|

Cost indicators of public

procurement risk assessment

|

|

5.

|

Cost at risk of cancellation of the procurement procedure

|

Quantile of the function of distribution of

the expected value of purchases that have been canceled, with the selected

level of confidence of 95%:

,

where: k is the absolute value of the quantile of the distribution of

a random discrete quantity, including  - the relative value; - the relative value;  - i-th value in

ascending order of the random variable; - i-th value in

ascending order of the random variable;  - estimation of the relative location of the

i-th value of a random variable in a set of its values; n - is the number of

values of the random variable under consideration. - estimation of the relative location of the

i-th value of a random variable in a set of its values; n - is the number of

values of the random variable under consideration.

|

|

6.

|

Cost at risk that the procurement procedure will not take place

|

Quantile of the function of distribution of the expected value of

purchases that did not take place

|

|

7.

|

Cost at risk of appealing the procurement procedure

|

Quantile function of the distribution of the expected value of the

procured purchases

|

|

8.

|

Cost at risk of disqualification of the participant

|

Quantile of function of distribution of the price offers sum for the

purchases which have been disqualified

|

|

9.

|

Aggregate value at risk

|

The amount of value at risk analyzed

|

|

10.

|

Cumulative public procurement risk indicator

|

Cumulative value at risk / Expected value of procurement

|

Source:

Pysmenna (2017)

We used the unique content for

analytical research in terms of sub-threshold and above-threshold procurement,

which is largely due to the availability of the necessary information (Prozorro, 2020). At the same time, we did not differentiate

according to the sectoral distribution of procurement customers.

All empirical data on individual

public procurement, reflected on ProZorro, were used.

We agree that at the organizational stage of their implementation,

public and private sector customers have differences (Beuve, Moszoro & Saussier, 2018). However,

audit evaluation according to our methodology can be used to determine the

effectiveness of public or private procurement. The reasoning in favor of this conclusion is the common rules for

conducting such procurement in the electronic system, on the basis of which we

conducted analytical research.

We have disregarded the detection by

analytical methods of conspiracy and/or corruption of procurement during

performance evaluation, although we agree with Lambert-Mogiliansky and Sonin

(2006) on the significance of such effects on procurement results. However,

methods of detecting fraud and its implications for procurement efficiency, the

risks of collusion and corruption have not been the subject of this article.

The purpose of the

study was to

propose a method of auditing the effectiveness of procurement procedures, which

links the indicators of efficiency, productivity, economy with the risks of

public procurement. To this end, the existing methods of assessing the use of

funds for public procurement and indicators that determine the factors

influencing the category of efficiency are analyzed. It was determined that a

comprehensive performance assessment is possible provided that a procurement

risk assessment is used.

4.

RESULTS

Scientific analysis proves that in a

broad sense, efficiency is an indicator that characterizes the relationship

between the result of the process and the cost of its implementation. In

addition, given the variety of targets and outlined results, it is possible to

qualify economic, social, production and other types of efficiency.

In view of the above, the efficiency

of the public procurement system should be understood as a complex concept

consisting of the following components:

first,

the target efficiency as the degree of achievement of the system results;

second,

economic efficiency as the ratio of the economic effect and the cost of

resources needed to achieve such an effect;

third, organizational efficiency,

which characterizes the infrastructural and competitive environment of order

placement, the level of development, implementation and use of regulatory,

methodological, informational, analytical support of the public procurement

system;

fourth, the efficiency of budget

expenditures for public procurement (Figure 1).

Emphasizing the application of the

method of comparing the costs and benefits of public procurement, it should be

noted that expert assessment of all costs play an important role. The latter

can be divided into direct, such as the contract price and insurance costs, and

indirect, arising from the occurrence of any adverse events.

Figure 1:

Decomposition of the definition “efficiency of the public procurement system”

Source:

developed by the authors

If

the benefits to the public or, in other words, the benefits of meeting needs

are higher than the cost

of purchasing and placing an order, then such a project is considered

potentially effective (Arrowsmith, Linarelli & Don Wallace, 2000). In this case, the cumulative effect of public procurement can be expressed

through various effects (Table 2).

Table 2: Features

of the set of effects

|

No

|

Types of effects

|

The essence of the concept

|

|

1.

|

Direct savings

|

are lower prices compared to the planned amount of funding

|

|

2.

|

Indirect or implicit savings

|

are characterized by the purchase of goods, works and services of

higher quality and on more favorable terms than usual. For example, no

advance payment, reduction of delivery time, longer warranty period,

availability of additional services, etc.

|

|

3.

|

The side effects

|

are manifested, for example, in reducing the level of corruption,

increasing the degree of openness of public procurement procedures,

increasing the business reputation of the customer and the investment

attractiveness of the region

|

Source: compiled by the

authors using Lapin, Kiseleva and Kumundzhieva (2016)

The costs of achieving the economic

effect of public procurement are usually expressed in the amount of:

·

labor

costs for the implementation of organizational measures for procurement;

·

material

costs of public procurement, such as the cost of consulting services,

consumables, postal and courier services, the cost of equipping workplaces and

renting additional premises, to ensure the functioning of the infrastructure of

the public procurement system (including official websites and publications),

training staff.

Waters (2015) considers it necessary

to take into account the degree of customer satisfaction when assessing the

effectiveness of procurement, i.e. compliance with consumer demands, ensuring

the best conditions for public procurement, reliability and qualification of

the supplier. In this case, we often use the method of comparison of suppliers,

which analyzes the proposals of all suppliers in order to identify those, who

are able to qualitatively fulfill the government order with the lowest contract

price.

However, in our opinion, there is an

important problem of information asymmetry, because only suppliers know their

true so-called “cost curves”. It is clear that under such conditions, customers

can analyze the history of relationships with suppliers, which is the most

effective tool for obtaining information on their costs for the amount of losses

due to the supply of substandard products, the number of erroneous deliveries,

reliability of delivery, etc.

It is possible to eliminate these

shortcomings in the case of using another assessment method of procurement efficiency - the method of

analysis of the main provisions of the contract. This method involves analyzing

the presence and essence of certain provisions that govern the relationship

between supplier and customer. In this case, the evaluation is based on certain

criteria that must be taken into account in the contract, namely: the presence

of possible risks during procurement, achieving a certain result given the

identified planned costs, delineation of rights and obligations of the parties,

establishing a monitoring procedure for orders, features of the dispute

resolution process, opportunities for communication between the parties, etc.

Thus, the contract is evaluated in terms of its completeness: the more detailed

are all the necessary provisions, the more efficient is the procurement.

Of course, the analysis of the

contract implementation can be carried out both during the whole cycle of

public procurement and after its completion. The analyzed method uses a number

of qualitative indicators, such as staff qualifications, the process of interaction

and communication, the degree of satisfaction of all parties involved in the

public procurement process, compliance with the deadlines for placing orders

and work.

Such an assessment is usually

conducted by questioning all participants, from senior management of the

authorized body for the coordination of procurement of goods, works and

services at public expense, suppliers, and ending with employed officials who directly

place orders or submit proposals for public procurement (Perov, Dashkov &

Abdrakhimov, 2006). The methodology for assessment the

public procurement systems MAPS (2018) of the World Bank and the Organization

for Economic Cooperation and Development (OECD) is scientifically meaningful.

The MAPS methodology was developed

in 2003-2004 and is constantly being improved, taking into account the

Recommendations of the OECD Public Procurement Council (RPP, 2015) and reflecting the leading international framework for such

procurement, in particular the Model Law of the United Nations Commission on

International Trade (Uncitral, 2011), EU Public Procurement Directives (Public Procurement in the EU, 2016).

The MAPS analytical structure

consists of a basic evaluation methodology and various additional modules,

focuses on specific aspects of public procurement policy and can be used by

countries depending on their needs. Thus, the analysis of the country’s

conditions Moncrieffe, Luttrell (2005) should be based on a limited number of

factors potentially important for procurement reforms, namely:

1) political, economic and geostrategic

situation in the country;

2) links between the procurement system

and public administration and public finance management systems,

3) national policy objectives that

affect the strategy, quantity and quality of public procurement (White,

Parfitt, Lee & Mason-Jones, 2016);

4) the environment for the

implementation of reforms in the field of public procurement.

The originality of the MAPS methodology

is that the system of indicators is based on four panels:

a) the existing legal and political

structures that regulate the procurement process in the country;

b) institutional framework and

management efficiency;

c) the system functioning and the

competitiveness of the internal market;

d) accountability, integrity and

transparency of the procurement system.

Each panel, in turn, includes

several indicators and sub-indicators to be evaluated. In total, such a system

has 14 indicators and 55 sub-indicators, which correspond to the relevant

criteria for “instant” comparison of the current system with these principles.

The studied indicators are expressed in qualitative and/or quantitative terms.

What are the advantages of the

method of evaluating the effectiveness of public procurement by MAPS? The

analysis carried out in the process of scientific research made it possible to

identify the following advantages of this technique:

·

first,

the formulation of the concept of “sustainable public procurement” in line with

the integration of the three components of sustainable development, i.e.

economic, social development and environmental protection (Spiller et al., 2013);

·

secondly,

public procurement objectives are usually aimed at reducing the demand for

resources, minimizing the negative impact of goods, works or services

throughout their life cycle, ensuring fair contract conditions, including

ethical rights, human rights and employment standards;

third,

the possibility of using public procurement and other innovative methods in

evaluation.

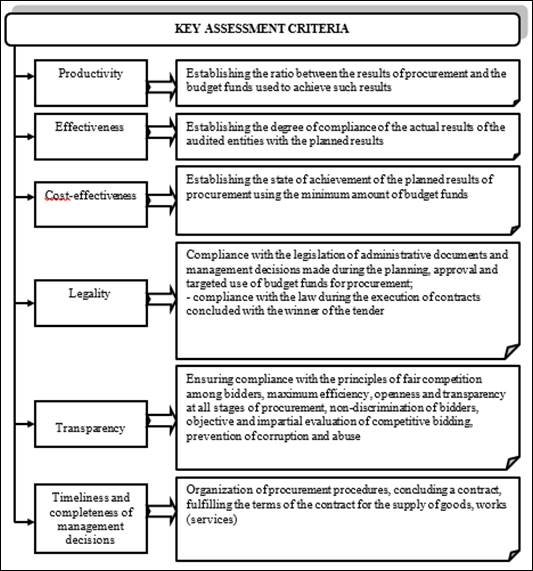

In practice, the audit evaluation of

public procurement uses evaluation criteria that do not take into account

public requests for information about their effectiveness (Figure 2). Under the

procurement audit by the Accounting Chamber (Accounting Chamber of Ukraine,

2019), the conclusions on the criteria of transparency, timeliness and

completeness of management decisions were not evaluated in terms of their

impact on the effectiveness of procurement procedures.

In

our opinion, the assessment of the public procurement effectiveness mainly in

terms of budget savings (in absolute terms and as an average percentage

reduction in the price of goods, works, services purchased) is insufficient for

audit purposes. This conclusion is made by the auditors of the Accounting

Chamber of Ukraine, assessing the report of the Ministry of Economy, Trade and

Agriculture of Ukraine (Accounting Chamber, 2020), in which

the Ministry informs about “savings” of 1.02 billion UAH in public procurement

in 2019, but does not indicate the causes of this process. The auditors of the

Accounting Chamber do not confirm the amount of public savings announced by the

Ministry of Economy, as there is no analysis and reliable indicators of

efficient and transparent public procurement, the report does not analyze the

factors, including those affecting the expected value of tenders.

In our opinion, the use of public

savings as the main criterion for the effectiveness of the public procurement

system is insufficient for an objective and comprehensive assessment, as the

calculation of budget savings does not take into account a reasonable

determination of the initial (maximum) contract price and pricing, resulting in

the problems in calculating the savings rate.

Figure 2: Criteria for assessing the

effectiveness of the use of public funds allocated for the purchase of goods,

works and services

Source: compiled by the

authors

It should be added that the analyzed

approach to assessing the effectiveness of public procurement by the only

criterion of saving budget resources, in our opinion, is not entirely correct.

This conclusion is substantiated by:

·

first,

insufficient development of methodological support in terms of calculating the

initial contract price;

·

secondly,

the leveling of attention to the specifics of non-price factors that affect

both the choice of supplier and terms of supply, and the level of qualification

and reliability of public procurement executors;

·

third,

not taking into account the costs of ensuring the functioning of the public

procurement system.

One cannot but agree that the

calculation of savings depends on the initial contract price.

At the same time, in case of

substantiation of the latter, it is necessary to have special knowledge of

market research in order to conduct an in-depth market research by public

customers. Therefore, in most cases, the initial (maximum) price of contracts

is fixed at the level of financial resources allocated for the purchase of a

particular type of product, which, in turn, does not reflect the real market

situation. But, under such conditions, when achieving the effect of saving

budget resources, there is usually a problem of incomplete use of allocated

budget funds for certain items. For the customer, this means a reduction in

funding for the costs in subsequent periods.

In addition, it should be noted that

significant savings can be achieved either as a result of unreasonable

overestimation of the initial contract price, or as a result of non-fulfillment

of public procurement plans and the presence of tenders, which did not lead to

the conclusion of such contracts.

Thus, the traditional assessment of

procurement efficiency based on the definition of budget savings does not fully

reflect the degree of procurement efficiency and can be used only for

operational analysis. Achieving savings of budget resources in public

procurement is, although the main, but still only a part of the holistic

process of efficient spending of budget funds, so it can be used only as an

additional criterion of efficiency. Such an assessment levels out a set of

important indicators, in particular - the quality of the customer’s planning

work, discipline in the execution of contracts, compliance with the principle

of competitive procurement, the customer’s compliance with the requirements of

public procurement legislation, etc.

Thus, the efficiency of public

procurement is replaced by the saving of budgetary resources, while the

efficiency of their spending includes their saving. Hence, it is clear that

such an assessment will determine only one aspect of the effectiveness of

public procurement.

We believe that the lack of

assessment of the risks faced by bidders and procurement customers is a

significant disadvantage of this approach, because determining the level of

such risks makes it possible to form additional characteristics of the

effectiveness of the public procurement system. In our opinion, the key risks

of public procurement that need to be evaluated and monitored are:

·

risk

of cancellation of the procurement procedure;

·

risk

that the procurement procedure will not take place;

·

risk

of procurement appeal;

·

risk

of disqualification of the participant.

Risk assessment, or in other words,

determining the quantitative and qualitative consequences of its

implementation, is possible using various statistical methods.

In our opinion, by using one or

another method of risk assessment, the following information about the risk can

be obtained: first, its probabilistic characteristics; secondly, its

quantitative assessment (Shevchuk, 1998):

|

|

(1)

|

where, - the value of the assessment

of the consequences of the occurrence of a risky event;

- function of parameter (x);

- function of parameter (x);

P - the

probability of a risky event;

I - the potential consequences of risk.

Risk assessment methods, which are traditional

and well-tested (Goncharenko & Filin, 2016) to evaluate the risks of public

procurement should be supplemented by the method of cost-effectiveness

assessment (Zaiets, 2017). It involves comparing the benefits and costs of

participation in the competitive public procurement procedures. In the field of public procurement, risk assessments can be obtained using the methods presented in Figure 3.

Figure 3: Methods for assessing the risks of

public procurement

Source: authors’ development

The results of the assessment of the

probabilities of risks realization are summarized and illustrated in Figure 4. Based on the performed calculations, it can

be concluded that the risk that the procurement procedure will not take place

is the highest risk of public procurement.

Figure 4: Probabilistic characteristics of

public procurement risks

Source: calculated by the

authors

The level of this risk reached 45%

in January 2018 on both sub-threshold and above-threshold procurement and most

of the time during 2018-2019 remained at a level above 35%. At the end of the

year, all types of risks were reduced.

The risk of disqualification of

public procurement participants is the second risk most likely to be realized.

The level of this risk is higher in

above-threshold procurement (from 15% to 30%) against sub-threshold procurement

(from 10% to 20%). This is due to the fact that the qualification requirements

for participants are much higher in the implementation of above-threshold

procurement. Risk assessments have been calculated using a similar approach.

In order to objectively assess and

characterize the level of risks of public procurement, relative to the total

expected value of public procurement in terms of sub-threshold and

above-threshold values, we calculate VaR-indicators of public procurement (risk

value indicators) equal to the quantile of the value distribution function

procurement at the selected confidence level of 95%.

Since the determination of VaR is

possible for quantities with a normal function of distribution of their values,

in order to check whether the distribution of values of the expected value of

public procurement can be considered normal, we calculated tables of

frequencies of distribution of the expected value of procurement.

The results of calculations of

quantitative assessments of public procurement risks for above-threshold

procurement are summarized in Table 3 and sub-threshold procurement - in Table

4.

Table

3: Statistical estimates of the cost characteristics of public procurement

risks in above-threshold procurement

|

Indicators

|

Risk of cancellation of the

procurement procedure

|

Risk that the procurement

procedure will not take place

|

Risk of appealing the

procurement procedure

|

Risk of disqualification of

the participant

|

|

2018

|

|

Average value of risk assessment

|

522522891,09

|

468289944,77

|

161540793,22

|

30369610571,04

|

|

The

standard deviation of the cost estimate of risk

|

475977186,07

|

494551086,83

|

196395124,37

|

73913648117,30

|

|

Variation of the cost estimate of risk

|

91,09%

|

105,61%

|

121,58%

|

243,38%

|

|

2019

|

|

Average value of risk assessment

|

745970646,78

|

1007978193,72

|

96946432,16

|

1312023241,27

|

|

The

standard deviation of the cost estimate of risk

|

699553623,49

|

609072408,93

|

63621341,81

|

724218388,76

|

|

Variation of the cost estimate of risk

|

93,78%

|

60,43%

|

65,63%

|

55,20%

|

|

2018-2019

|

|

Average value of risk assessment

|

475543722,49

|

509924334,26

|

137714986,33

|

13018768698,69

|

|

The

standard deviation of the cost estimate of risk

|

587119348,44

|

617085748,07

|

159853292,97

|

48649237510,91

|

|

Cost

at risk, VAR

|

1441269112

|

1524940065

|

400650255

|

93039643467

|

|

The total value at risk

|

96406502899

|

|

Cumulative risk of public procurement

|

47,85%

|

Source: authors’ calculations

Table 4: Quantitative risk

assessments of public procurement in sub-threshold procurement

|

Indicators

|

Risk of cancellation of the

procurement procedure

|

Risk that the procurement

procedure will not take place

|

Risk of appealing the

procurement procedure

|

Risk of disqualification of

the participant

|

|

2018

|

|

Average value of risk assessment

|

4526153302,26

|

4738741838,41

|

4339546073,76

|

3830891947,16

|

|

The

standard deviation of the cost estimate of risk

|

6656071484,08

|

4625735620,49

|

8729026880,50

|

3259557149,33

|

|

Variation of the cost estimate of risk

|

147,06%

|

97,62%

|

201,15%

|

85,09%

|

|

2019

|

|

Average value of risk assessment

|

5733219792,15

|

8573202986,72

|

6081006510,89

|

18654570799,30

|

|

The

standard deviation of the cost estimate of risk

|

4301519882,77

|

2441631225,58

|

3469600566,59

|

29250724848,36

|

|

Variation of the cost estimate of risk

|

75,03%

|

28,48%

|

57,06%

|

156,80%

|

|

2018-2019

|

|

Average value of risk assessment

|

5190039871,70

|

6847695469,98

|

5297349314,18

|

11983915315,84

|

|

The

standard deviation of the cost estimate of risk

|

5363959804,53

|

3997205454,98

|

6261664278,55

|

22628308940,75

|

|

Cost

at risk, VAR

|

14012968611,00

|

13422513360,28

|

15596870513,50

|

49204171348,81

|

|

The total value at risk

|

92236523833,60

|

|

Cumulative risk of public procurement

|

12,05%

|

Source: authors’ calculations

As these data show, the total risk

of above-threshold public procurement in 2018-2019 is 47.85%, while the total

risk of the sub-threshold public procurement in 2018-2019 is equal to 12.05%.

In order to assess the value of the

aggregate risk indicator of public procurement, we suggest using the classical

approach, which involves the allocation of four risk zones depending on the

indicator values (Table 5).

Table

5: Gradation of risk zones depending on the values of the aggregate risk

indicator

|

The value of the aggregate

risk indicator

|

Risk Zone

|

|

0 – 0,1

|

Minor risk

|

|

0,1 – 0,3

|

Permissible risk

|

|

0,3 – 0,6

|

Increased risk

|

|

> 0,6

|

Unacceptable risk

|

Source: Stupakov and Tokarenko (2005)

In our opinion, such a scale is

acceptable for assessing the public procurement effectiveness. Therefore,

according to these criteria, the aggregate risk of above-threshold public

procurement is increased, while the aggregate risk of sub-threshold public

procurement is insignificant.

Thus,

the aggregate risk in above-threshold procurement is increased due to the high

probability that, firstly, the procurement procedure will not take place and,

secondly, the disqualification of participants.

For

audit purposes, this necessitates the adjustment of the scope of audit

procedures, which depend on the assessed risk of the audited entity.

The estimated risk of individual

procurement procedures according to the above method can be used when

identifying the effectiveness of the organization of procurement by individual

regions (periods).

Thus, the quantitative and cost

analysis of risk assessment in this case is carried out on the basis of

selected analytical data of the Prozorro system of territories, or one or a

group of customers.

5.

CONCLUSIONS AND RECOMMENDATIONS

Estimation of efficiency Performance management

will vary significantly from one context or situation to another, so adapting

general approaches to determining the effectiveness of the use of public funds

requires methodologies that would answer the questions of specific situations

“What are the generative mechanisms of this particular design of PMS?” and “How

do they interact with the particular context?” (Pollitt, 2013).

The research methodology is based on

the application of statistical and analytical methods on the data on the

conducted procurement procedures during 2018-2019.

In Ukraine, the operation of an open

electronic public procurement system has created a unique opportunity for

accessible analytics in the context of all announced procurement procedures.

The calculations were performed in

terms of sub-threshold and above-threshold procurement. The total amount of

processed data for 2018 is 1.084 million procurement procedures, and for 2019 -

1.238 million procurement procedures, which is 100% of the declared procurement

procedures for this period. Based on the results of the study, it is proposed

to supplement the existing methods of assessing procurement risk indicators to

conduct an audit assessment of procurement effectiveness.

Procurement efficiency was assessed

via four types of risk: the risk of cancellation of the procurement procedure,

the risk that the procurement procedure will not take place, the risk of

appealing the procurement, the risk of disqualification of the participant

separately for sub-threshold and above-threshold procurement. The riskiest

periods of procurement were established and the aggregate risk indicator of

public procurement was calculated at the level of 47.85%. This enabled

assessing the impact of certain types of risk on the procurement effectiveness

and adjusting the scope of audit procedures to verify individual procurement.

We see the further direction of the

research in determining the risks of procurement by types of selected

procedures, which will generate analytical data for risk management in the

supply chain management.

REFERENCES

Accounting Chamber (2019). Report on the analysis of the functioning of the public procurement

system. Available:

https://rp.gov.ua/upload-files/Activity/Collegium/2019/12-2_2019/Zvit_12-2_2019.pdf.

Access: 1th April, 2020.

Accounting

Chamber (2020). Information on

«Savings» of UAH 28.2 billion in public procurement in 2019 is contradictory. Available: https://rp.gov.ua/PressCenter/News/?id=908.

Access: 6th April, 2020.

Adi, S., & Dutil, P. (2018). Searching for

strategy: Value for Money (VFM) audit choice in the new public management era. Canadian Public Administration, 10.1111/capa.12254, 61(1),

(91-108). DOI: https://doi.org/10.1111/capa.12254.

Antoniuk, O., Chyzhevska, L., & Semenyshena, N. (2019). Legal

regulation and trends of audit services: what are the differences (evidence of

Ukraine). Independent Journal of

Management & Production, 10(7),

673-686. DOI: http://dx.doi.org/10.14807/ijmp.v10i7.903

Antoniuk, O., Kuzyk,

N., Zhurakovska, I., Sydorenko, R., & Sakhno, L. (2020).

The Role of «Big Four» Auditing Firms in the Public Procurement Market in

Ukraine. Independent Journal of Management &

Production, 11(9), 2483-2495.

DOI: http://dx.doi.org/10.14807/ijmp.v11i9.1432.

Arrowsmith, S., Linarelli, J., & Don

Wallace, JR. (2000). Regulating Public

Procurement. National and International Perspectives. Kluwer Law International.

Beuve, J.,

Moszoro, M. W., & Saussier, S. (2018). Political contestability and public

contract rigidity: An analysis of procurement contracts. Journal of Economics & Management Strategy.

doi:10.1111/jems.12268.

Bowerman, M., Raby, H., & Humphrey, C.

(2000). In Search of the Audit Society: Some Evidence from Health Care, Police

and Schools. International Journal of

Auditing, 4(1), 71–100.

DOI:10.1111/1099-1123.00304.

Duncombe, W.,

& Searcy, C. (2007). Can the Use of Recommended Procurement Practices Save

Money? Public Budgeting & Finance, 27(2), 68–87. DOI:10.1111/j.1540-5850.2007.00875.x.

Fesenko, V., Vakulchyk,

O., Guba, O., Ostapchuk, S., & Babich, I. (2020). The Results

of Implementation of European Requirements in Management of Transfer Pricing

Audit (Experience of Ukraine). Independent Journal of Management &

Production, 11(9), 2417-2434. DOI:

http://dx.doi.org/10.14807/ijmp.v11i9.1412.

Goncharenko, L. P., & Filin, S. A. (2016). Risk management. Moscow: KNORUS.

Ivanova, O. V.

(2010). Methodology for a comprehensive assessment of the

effectiveness of public procurement of the Oryol region. Bulletin of TulSU. Economic and legal sciences, 2, 183-192.

Karlöf,

B. (1996). New age efficiency and demands on organizations. Strategic Change, 5(1), 43–48.

DOI:10.1002/(sici)1099-1697(199601)5:1<43::aid-jsc211>3.0.co;2-a.

Khorunzhak, N., Belova, I., Zavytii, O.,

Tomchuk, V., & Fabiianska, V. (2020). Quality Control of

Auditing: Ukrainian Prospects. Independent Journal of Management & Production, 11(8), 712-726. DOI: dx.doi.org/10.14807/ijmp.v11i8.1229.

Khorunzhak, N., Brukhanskyi, R., &

Ivanyshyn, V. (2019). Logic-statistical information models in control function of accounting. Independent Journal of Management & Production, 10(7), 846-871. DOI: http://dx.doi.org/10.14807/ijmp.v10i7.906.

Kroll, Y.,

& Levy, H. (1980). Sampling Errors and Portfolio Efficient Analysis. Journal of Financial and Quantitative

Analysis, 15(3), 655-688. DOI:10.2307/2330403.

Lambert-Mogiliansky, A., & Sonin, K. (2006).

Collusive Market Sharing and Corruption in Procurement. Journal of Economics Management Strategy, 15(4),

883–908. doi:10.1111/j.1530-9134.2006.00121.x.

Lapin, A. E.,

Kiseleva, O.V., & Kumundzhieva, E. L. (2016). Approaches to assessing the

effectiveness of the contract system in the field of state and municipal

procurement. Business. Education. Right.

Bulletin of the Volgograd Institute of Business, 11(34), 30-35.

MAPS (2018). Methodology for Assessing

Procurement Systems. Available: http://www.mapsinitiative.org/methodology/MAPS-methodology-for-assessing-procurement-systems.pdf. Access: 18th June, 2020.

Mayne, J., & Ontario, O. (2006).

Audit and evaluation in public management: challenges, reforms, and different

roles. The Canadian Journal of Program

Evaluation, 21(1),

11–45.

McCrae, M., &

Vada, H. (1997). Performance Audit Scope and the Independence

of the Australian Commonwealth Auditor‐General. Financial Accountability & Management, 13(3). DOI: https://doi.org/10.1111/1468-0408.00034.

Melnyk, N.,

Trachova, D., Kolesnikova, O., Demchuk, O., & Golub, N. (2020).

Accounting Trends in the Modern World. Independent

Journal of Management & Production,

11(9), 2403-2416. DOI:

http://dx.doi.org/10.14807/ijmp.v11i9.1430.

Methodological

(2008). Methodological recommendations

for assessing the effectiveness and transparency of placing state and municipal

orders. Moscow: Delovoy dvor.

Moncrieffe, J.,

& Luttrell, C. (2005). Аn analytical framework for understanding the political economy of

sectors and policy arenas. Overseas Development

Institute. Availiable:

http://www.odi.org/sites/odi.org.uk/files/

odi-assets/publications-opinion-files/3898.pdf. Access:

1th MarchMay, 2020.

Nesterovich, N. V. (2008). N. 94-FZ: how to find savings. State order: Management, Placement, Provision. 12 (April, June), 32–35.

Pasko, O., Melnychuk, O., & Bilyk T. (2019).

Ownership concentration, investor protection and economic performance in public

agroindustrial companies with the listing on Warsaw stock exchange. Independent Journal of Management &

Production, 10(7), 817-845. DOI: http://dx.doi.org/10.14807/ijmp.v10i7.914.

Perov, K. A.,

Dashkov, S. B., & Abdrakhimov, D. A. (2006). Development of a methodology for calculating the

economic efficiency of placing orders for the supply of goods, performance of

work, provision of services for state and municipal needs: research report. Moskow: LTD Institute of Competitive Technologies.

Pollitt, C.

(2013). The logics of performance management. Evaluation, 19(4),

346–363. DOI: https://doi.org/10.1177/1356389013505040.

Pollitt, C., Girre, X., Lonsdale, J., Mul, R.,

Summa, H., & Waerness, M. (1999). Performance or Compliance? Performance Audit and Public Management

in Five Countries. Oxford: Oxford University Press.

Prozorro

(2020). ProZorro is a

hybrid electronic open source government e-procurement system. Available: https://prozorro.gov.ua/ Access: 5th

June, 2020.

PUBLIC

PROCUREMENT IN THE EU (2016). Public Procurement in the EU: Legislative Framework, Basic

Principles and Institutions. Available: http://www.sigmaweb.org/publications/Public-Procurement-Policy-Brief-1-200117.pdf .

Access: 1th November, 2018.

Pyismenna, M. (2017). Written by MS

State audit and analysis of public procurement: theory, methodology and

practice. Kyiv: Center for Educational Literature.

Rodrigues, P. C. C., & Semenyshena, N.

(2019). Editorial Introduction. Independent

Journal of Management & Production, 10(7), 911-914. DOI: http://dx.doi.org/10.14807/ijmp.v10i7.775.

Rodrigues, P. C. C., & Semenyshena, N.

(2020). Special Edition (Integration System of Education, Science and

Production) Introduction. Independent

Journal of Management & Production, 11(8), 801-806. DOI:

http://dx.doi.org/10.14807/ijmp.v10i7.775

Rodrigues, P. C. C., Simanaviciene, Z., & Semenyshena, N. (2020). Editorial Volume

11, Issue 9. Independent

Journal of Management & Production, 11(9), 2542-2547. DOI:

http://dx.doi.org/10.14807/ ijmp.v11i9.1424

RPP (2015). Recommendation on Public Procurement: Public Procurement is the

cornerstone of strategic governance. Available: http://www.oecd.org/gov/public-procurement/recommendation/OECD-Recommendation-on-Public-Procurement.pdf. Access: 24th April, 2020.

Semenyshena, N., Khorunzhak, N., & Zadorozhnyi, Z.-M.

(2020). The

Institutionalization of accounting: the impact of national standards on the

development of economies. Independent

Journal of Management & Production, 11(8), 695-711. DOI:

https://doi.org/10.14807/ijmp.v11i8.1228.

Semenyshena, N.,

Sysiuk, S., Shevchuk, K., Petruk, I., & Benko, I. (2020). Institutionalism

in Accounting: a Requirement of the Times or a Mechanism of Social Pressure? Independent Journal of Management &

Production, 11(9), 2516-2541.

DOI: http://dx.doi.org/10.14807/ijmp.v11i9.1440.

Shevchuk, V. O. (1998). Control of economic systems in a society in transition (problems of

theory, organization, methodology). Kyiv: Kyiv State University of Trade

and Economics.

Slobodyanik, Y., Kondriuk, L., & Haibura,

Y. (2019). The Strategy of Institutional Reform of the Supreme Audit

Institution: the Case of Ukraine. Independent

Journal of Management & Production, 10(7). DOI: http://dx.doi.org/10.14807/ijmp.v10i7.916.

Sollish,

F., & Semanik, J. (2012). The Procurement and Supply Manager's Desk Reference. Chapter 4 Supplier Selection Criteria Book Editor(s): Wiley. DOI: https://doi.org/10.1002/9781119205098.ch4.

Spiller, P., Reinecke, N., Ungerman, D., &

Teixeira, H. (2013). Procurement 20/20: Supply

Entrepreneurship in a Changing World. In: Chapter 7 The New Economic Drivers: Capturing the

Total Impact of Environmental, Social, and Regulatory Factors, ch. 7. DOI: https://doi.org/10.1002/9781119204985.ch7.

Stupakov, V. S., & Tokarenko, G.S. (2005). Risk management. Moscow:

Finance and Statistics.

Uncitral (2011). Model

Law on Public Procurement. Available: https://uncitral.un.org/en/texts/procurement/modellaw/public_procurement. Access: 7th June, 2020.

Vdovenko, N., Piven,

A., Radchenko, O., Sinenok, I., & Voskobiinyk, S. (2020). Institutional Environment for Financial

Provision of Small Agricultural Business Entities of Ukraine. Independent Journal of Management &

Production, 11(9), 2379-2402.

DOI: http://dx.doi.org/10.14807/ijmp.v11i9.1419.

Waters, D.

(2015). Logistics. Supply chain management. Logistics. An

Introduction to Supply Chain Management. Moscow: UNITY-DANA.

White, G. R.

T., Parfitt, S., Lee, C., & Mason-Jones, R. (2016).

Challenges to the Development of Strategic Procurement: A Meta-Analysis of

Organizations in the Public and Private Sectors. Strategic Change, 25(3), 285–298. DOI:10.1002/jsc.2061.

Zaiets, N. M. (2017). A pilot analysis of the

procurement procedures. Bulletin of ZhDTU. Series: Economics of Science, 1(179), 72-80.

AUDIT

ASSESSMENT OF THE EFFECTIVENESS OF PUBLIC PROCUREMENT PROCEDURES

AUDIT

ASSESSMENT OF THE EFFECTIVENESS OF PUBLIC PROCUREMENT PROCEDURES